High-income earners face a problem most financial media never address honestly: once you’re earning $500K or more, the standard playbook runs dry fast. Max your 401(k), harvest some losses, maybe do a backdoor Roth — and you’re still writing enormous checks to the IRS. What most advisors never bring up is one of the most powerful tax reduction tools in the entire U.S. tax code: oil and gas investing.

This isn’t a fringe strategy. Intangible drilling cost (IDC) deductions have been codified in the tax code since 1917. They exist because the federal government actively wants capital deployed into domestic energy production — and it rewards investors who do so with some of the most favorable tax treatment available to private investors.

In this article, we break down the advanced oil and gas tax strategies we use at Prosperl CPA for our high-income clients — including how to combine oil and gas with real estate, use it for capital gains planning, supercharge a Roth conversion, shift income to family members, and deploy it inside a qualified opportunity zone fund for a potentially tax-free exit.

What You’ll Learn

- Why oil and gas losses are superior to nearly every other type of investment loss

- How intangible drilling costs work and what kind of deduction to expect

- The key differences between working interests, royalty rights, and fund structures

- How to stack oil and gas with real estate for compounding tax benefits

- How to use oil and gas to offset capital gains from stocks, RSUs, and real estate

- How to reduce the tax bite on a Roth conversion using energy investments

- Income shifting strategies for family members using oil and gas interests

- How the oil and gas qualified opportunity zone (QOZ) structure creates a tax-free exit

🎧 Episode 143 – Advanced Oil & Gas Tax Strategies (Exclusive Client Workshop Preview!)

Prefer to watch or listen?

Watch on YouTube: https://www.youtube.com/watch?v=VmIrnb6k3HA&t=2s Listen on Apple Podcasts: https://podcasts.apple.com/us/podcast/ep-143-advanced-oil-gas-tax-strategies-exclusive-client/id1604630028?i=1000761849359

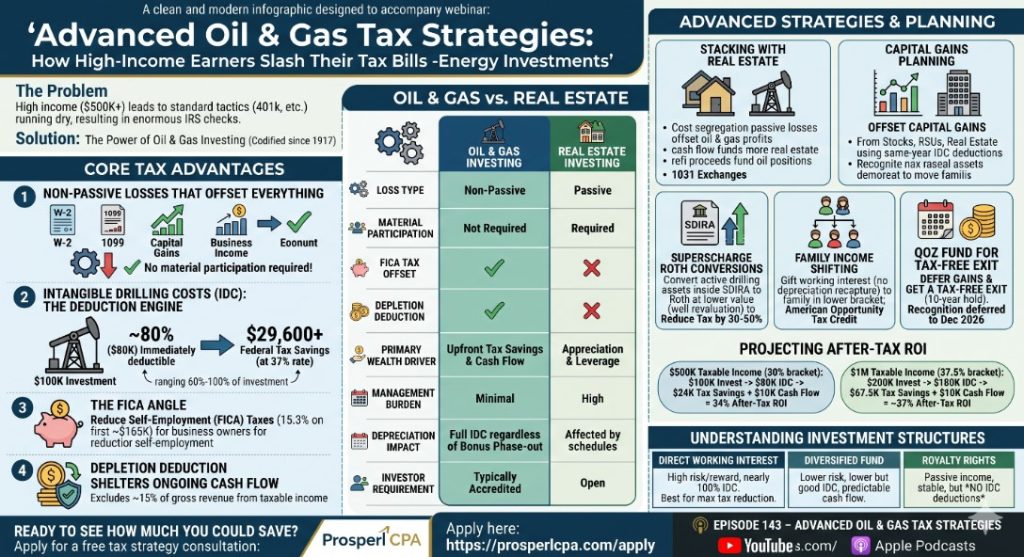

Why Oil & Gas? The Core Tax Advantages

Before getting into advanced strategies, let’s establish why oil and gas investing attracts high-income earners in the first place.

Non-Passive Losses That Offset Everything

The single most valuable feature of a properly structured oil and gas working interest is that the losses are non-passive. That designation is everything.

Most investment losses are passive and can only offset other passive income. Capital losses are capped. But non-passive losses — the kind generated by a working interest in oil and gas — can offset W-2 income, 1099 self-employment income, capital gains, interest income, and business income. No material participation requirements. No REP status test. No 750-hour threshold to clear. You invest, the deduction flows through, and it offsets your highest-taxed income.

Intangible Drilling Costs: The Engine of the Deduction

When you invest in a working interest, a substantial portion of your capital goes toward what the IRS classifies as intangible drilling costs — the expenses of drilling, excavating, and equipping a well. These costs are immediately deductible in the year incurred, typically ranging from 60% to 100% of your investment amount.

In practical terms: if you invest $100,000 into an oil and gas project with an 80% IDC allocation, you receive an $80,000 federal tax deduction that year. At a 37% marginal rate, that’s $29,600 in tax savings — on top of whatever cash distributions the investment generates.

The FICA Angle Most Advisors Miss

For business owners, sole proprietors, and 1099 earners, there’s an additional layer of benefit that almost no advisor discusses: oil and gas losses can offset self-employment taxes.

In 2025, the first approximately $165,000 of self-employment income is subject to FICA at 15.3%. An oil and gas deduction can reduce that base, effectively making each dollar of deduction worth 30–45% in combined federal and self-employment tax savings. For clients in states with no income tax or those who can’t benefit from S-corp salary structures, this is a significant lever.

Depletion Deduction Shelters Ongoing Cash Flow

Once the well is producing, you’re not done receiving tax benefits. A statutory depletion deduction allows investors to exclude approximately 15% of gross revenue from taxable income each year — a permanent, cash-free paper deduction that reduces the tax cost of ongoing distributions. You receive the cash flow, but only pay taxes on 85% of the revenue. In years when you reinvest, IDC deductions from new projects can offset even more of those profits.

Understanding the Investment Structures

The tax treatment of an oil and gas investment depends significantly on how it’s structured. Here are the three primary types:

Direct Working Interest in an Operator: You invest directly alongside the operator drilling a specific well or small group of wells. Higher risk, higher IDC deduction (often approaching 100%), higher potential return. Best for investors who want maximum tax reduction and can tolerate concentration risk.

Diversified Fund (Working Interest): Your capital is spread across 80–100 wells. The IDC deduction is somewhat lower, but the risk of a single well delay or underperformance is mitigated. Most appropriate for investors who prioritize tax efficiency with more predictable cash flow.

Royalty Rights: You own the land rights, not the drilling operation. The royalty income is passive and stable, but there are no IDC deductions — the risk/reward structure doesn’t qualify. Good for income stability; not a significant tax reduction vehicle.

Some funds blend currently producing wells (less risk, less deduction) with new drilling (more deduction, slightly more risk). Your mix determines the blend of tax benefit and cash flow predictability.

Projecting Your After-Tax ROI

Before any investment decision, we build a projection showing after-tax return — not just gross yield. Here’s the framework:

Example 1 — $500K taxable income, 30% federal bracket:

- Investment: $100,000

- IDC deduction (80%): $80,000

- Tax savings: $80,000 × 30% = $24,000

- Estimated year-one cash distributions: $10,000

- Total year-one return: $34,000 on a $100,000 investment = 34% after-tax ROI

Example 2 — $1M taxable income, 37.5% federal bracket:

- Investment: $200,000

- IDC deduction (90%): $180,000

- Tax savings: $180,000 × 37.5% = $67,500

- Estimated cash distributions: $10,000

- Total year-one return: ~37% after-tax ROI

The math gets more compelling the higher your bracket. And unlike stock market returns — which are volatile — the tax savings portion is reliable as long as the law remains unchanged. IDC deductions have survived every major tax overhaul since 1917 because they represent a bipartisan energy policy incentive, not a loophole.

Want to know how much you could save in taxes?

Apply for a free tax strategy consultation and we’ll show you exactly what’s possible based on your income and situation.

→ Apply here: https://prosperlcpa.com/apply

Oil & Gas vs. Real Estate: An Honest Comparison

Many of our clients are already deep into real estate investing. The question we frequently hear is: should I choose one or the other?

The answer is almost always: combine them.

Here’s how they compare across key dimensions:

Where real estate wins: Leverage and appreciation. With real estate, you borrow against the asset, benefit from long-term price appreciation, execute 1031 exchanges to defer gains indefinitely, and access equity through cash-out refinances tax-free. For clients focused on long-term wealth accumulation and intergenerational transfer, real estate remains a cornerstone strategy.

Where oil and gas wins:

- Non-passive losses that offset W-2 and self-employment income (real estate losses typically require REP status or short-term rental material participation to achieve the same result)

- No material participation required — truly passive

- FICA offset capability

- Depletion deduction on ongoing revenue

- High velocity of cash return (many clients see their capital returned within 18 months through combined tax savings and distributions)

- Bonus depreciation phase-outs don’t apply (IDC deductions remain at full value regardless of depreciation schedules)

- No landlord headaches, no HVAC calls on Sunday afternoons

For clients who love the concept of real estate investing but have concluded that active property management doesn’t fit their life — or who already have real estate but want to deploy additional capital without adding management burden — oil and gas is often the right next move.

Stacking Oil & Gas with Real Estate

The real power emerges when you use both strategies in coordination:

Using real estate losses to shelter oil and gas profits. In years when you’re not deploying new oil and gas capital (and therefore generating fewer IDC deductions), the profits from existing wells become taxable. That’s when a cost segregation study on a property in your real estate portfolio can generate passive losses to offset those passive profits — dollar for dollar. This creates a self-reinforcing cycle: real estate shelters oil and gas gains, oil and gas distributions fund more real estate, and cost segregation studies continue generating losses to offset the cycle.

1031 exchanges between oil and gas and real estate. This is underused and genuinely powerful. A capital gain from a real estate sale can be rolled into an oil and gas working interest via a 1031 exchange — and vice versa. It requires careful structuring (equal or greater value rules apply, and debt replacement can complicate real estate-side exchanges), so coordinate with us before executing. But for the right client, this eliminates a capital gain event and deploys the proceeds into a tax-advantaged income-producing investment.

Cash-out refinancing to fund oil and gas positions. If you have appreciated real estate and favorable refi terms, pulling equity out tax-free and deploying it into oil and gas can generate both new income and a significant IDC deduction. Yes, there’s an interest cost — but the combination of cash flow distributions and tax savings from the oil and gas investment often more than offsets it.

Oil & Gas for Capital Gains Planning

This strategy applies well beyond real estate. Any capital gains event — stock sales, RSU vesting events, business asset sales, even home sale gains over the exclusion — can be partially or fully offset using oil and gas IDC deductions.

Example: You sell $100,000 in Apple stock with a $50,000 gain. You receive $100,000 in proceeds. If you invest those proceeds into an oil and gas project with an 80% IDC rate, you generate an $80,000 non-passive deduction — which offsets your $50,000 capital gain and an additional $30,000 of ordinary income. The net tax impact of the stock sale is negative: you’ve reduced your total taxable income even after recognizing the gain.

For tech employees with concentrated RSU positions, employees receiving large bonuses, or any client approaching a significant liquidity event, this is a planning opportunity that should be modeled before the event, not after.

The Roth Conversion Angle: Reducing Your Conversion Tax by 30–50%

One of the most sophisticated applications we walk clients through is using an oil and gas investment held inside a self-directed IRA to reduce the tax cost of a Roth conversion.

Here’s the core mechanism: when you transfer oil and gas assets from a traditional IRA or 401(k) into a Roth IRA, the conversion is taxed on the fair market value of what’s being transferred at the time of the conversion. If the oil and gas investment is in active drilling phase — with capital deployed but the well not yet producing — the revalued asset is worth substantially less than what was invested. The IRS taxes the lower fair market value, not the original investment amount.

We’ve seen this strategy reduce the taxable portion of a Roth conversion by 30–50%. On a $100,000 conversion, that means potentially paying taxes on only $50,000–$70,000, while still moving the full $100,000 worth of underlying asset into tax-free Roth growth.

The long-term compounding math on that saved tax dollars — growing tax-free in the Roth over 20–30 years — can produce hundreds of thousands of dollars of additional wealth. This is a strategy that requires precise coordination and a qualified custodian, but for the right client, it’s transformative.

Income Shifting: Gifting Oil & Gas Interests to Family Members

Oil and gas investments have a unique gifting advantage: when you gift a working interest to a family member, there is no depreciation recapture triggered on the transfer. This stands in contrast to many business assets, where removing them from active use triggers recapture of prior deductions.

The strategy: Invest $100,000 into an oil and gas project in year one. Receive a $90,000 IDC deduction — reducing your taxes by $33,300+ at a 37% rate. In year two, gift the working interest to a family member (a parent, an adult child in college, a spouse in a lower bracket). That family member now holds a $100,000 investment generating ongoing distributions — taxed at their lower marginal rate, further reduced by the depletion deduction.

For children in college, this strategy pairs well with the American Opportunity Tax Credit, which requires the student to show some taxable income. Gifting an oil and gas interest to a college-age child can generate the modest taxable income needed to activate the credit (worth up to $2,500/year for four years), while keeping their overall tax bill minimal thanks to the standard deduction and depletion allowances.

Oil & Gas Qualified Opportunity Zone Funds: The Tax-Free Exit

Qualified opportunity zone (QOZ) funds represent one of the most powerful capital gains deferral and elimination tools in the tax code. When combined with oil and gas investing, they offer something few other structures can: a tax-free exit after a 10-year hold.

How the structure works:

- A capital gains event triggers a tax liability (from stocks, real estate, RSUs, or a business sale).

- You invest those gains into an oil and gas QOZ fund within 180 days.

- The capital gain recognition is deferred until December 2026 (or until you exit, if earlier).

- Because the fund invests in drilling operations, the land is revalued periodically — reducing the amount of gain recognized at deferral by an estimated 30%.

- The fund reinvests distributions into additional wells throughout the hold period, accumulating a growing portfolio of producing assets.

- After 10 years, you exit the fund entirely tax-free on all appreciation generated within the fund.

The annual cash yield inside the QOZ structure is modest — typically 6–8%, offset by IDC deductions — but the exit is where the real wealth creation occurs. As the fund accumulates more wells over a decade, the total portfolio value compounds. Selling after 10 years with zero capital gains tax on the full appreciation is the equivalent of a Roth IRA with no contribution limits and no age restrictions. It’s an elite-level strategy for clients facing large capital gains events who have a long investment horizon.

FAQ

Q: Are intangible drilling cost deductions safe from future tax law changes? IDC deductions have existed since 1917 and have survived dozens of tax reform efforts because they represent federal energy policy, not a loophole. No tax professional can guarantee permanence, but IDCs are among the most entrenched incentives in the code.

Q: Do I need to be an accredited investor to invest in oil and gas? Most working interest funds and direct operator investments require accredited investor status (generally $200K+ individual income or $1M+ net worth excluding primary residence). Royalty rights structures may have different requirements. Confirm with each provider.

Q: Can oil and gas losses offset my California state taxes? Generally no. If the oil and gas fund is domiciled in Texas or another state, California treats that activity as non-California source income. The losses will typically offset your federal taxes but not your California income taxes. However, because the IDC and depletion deductions still reduce the income statement of the investment, you may pay no California tax on the distributions either.

Q: How quickly do investors typically see cash returns? In direct working interest structures, many investors see their combined tax savings and cash distributions return their full investment within 18 months. This varies by project, operator, drilling timeline, and your tax bracket. Higher brackets compress the return timeline because the tax savings are larger.

Q: What is the excess business loss limitation and how does it affect me? For W-2 earners, there is a cap on how much business loss can offset non-business income in a given year (approximately $313,000 for individuals and $626,000 for married filing jointly in recent years — confirm current limits, as they adjust annually). Losses above this threshold carry forward and can offset future W-2 income. This limitation doesn’t eliminate the benefit; it spreads it across years.

Q: How do royalty rights differ from working interests for tax purposes? Royalty rights do not generate IDC deductions because you’re not participating in the drilling risk — you simply collect land rent. Royalty income is passive and taxed favorably, but it is not a significant tax reduction vehicle. Working interests are what generate the large non-passive losses.

Q: Can I hold oil and gas in a self-directed IRA? Yes. The main tradeoff is that IDC deductions are absorbed within the IRA and do not reduce your personal taxable income in the contribution year. The primary purpose of holding oil and gas in a self-directed IRA is to reduce the fair market value of assets being converted to a Roth — effectively reducing the taxable portion of the Roth conversion. This is a sophisticated strategy best executed with specialist guidance.

Q: Do I need to vet investment providers myself? We make introductions to operators and fund managers we know and trust, but the final investment decision is always yours. Performing your own diligence — reviewing the investment deck, confirming well locations, checking production data (which is often public record), and understanding the distribution schedule — is advisable before committing capital.

Key Takeaways

- Oil and gas working interests generate non-passive losses that offset W-2 income, capital gains, business income, and in some cases FICA taxes — making them uniquely versatile compared to passive real estate losses.

- Intangible drilling costs (IDCs) typically represent 60–100% of your investment amount and are deductible in the year of investment, creating substantial upfront tax reduction.

- A depletion deduction shelters approximately 15% of gross production revenue from tax each year — permanently reducing the effective tax rate on ongoing distributions.

- Oil and gas combined with real estate creates a compounding tax strategy: cost segregation losses offset oil and gas profits; oil and gas distributions fund more real estate; refinancing proceeds fund more oil and gas positions.

- Capital gains from any source — stocks, RSUs, real estate, business sales — can be offset using IDC deductions in the same tax year.

- A self-directed IRA strategy using oil and gas can reduce the taxable portion of a Roth conversion by 30–50%, with the tax savings compounding tax-free over decades.

- Gifting oil and gas interests to family members in lower tax brackets is a clean income-shifting strategy with no depreciation recapture, unlike most business asset transfers.

- Oil and gas QOZ funds defer capital gains, partially reduce the recognized gain at deferral, and offer a completely tax-free exit after a 10-year hold — effectively functioning as a Roth IRA with no contribution limits.

- After-tax ROI on oil and gas investments often exceeds 30–37% in year one for high-bracket investors — far exceeding the risk-adjusted returns of most conventional investment vehicles when tax savings are properly accounted for.

Ready to See How Much You Could Save?

Apply for a free tax strategy consultation: → https://prosperlcpa.com/apply

Not ready yet? Start with our free Tax Planning Checklist and mini-course: → https://taxplanningchecklist.com

This article is adapted from Episode 143 of the Mark Perlberg CPA Podcast.

Watch on YouTube: https://www.youtube.com/watch?v=VmIrnb6k3HA&t=2s Listen on Apple Podcasts: https://podcasts.apple.com/us/podcast/ep-143-advanced-oil-gas-tax-strategies-exclusive-client/id1604630028?i=1000761849359