If you’re a high-income earner in California, you already know taxes are painful. But most people don’t realize how painful — or exactly how much worse it gets as your income climbs. This article breaks down the real numbers, threshold by threshold, and shows what’s actually possible to do about it.

What You’ll Learn

- How California’s progressive tax system works — and what’s hidden inside it

- Exactly how much a married couple pays in state and federal taxes at $300K, $400K, $500K, $750K, $1M, and $1.5M

- Why your raise might feel like a 50% pay cut at higher income levels

- Which tax reduction strategies work in California — and which ones don’t

- How to go from a 42% blended rate down to 17% without leaving the state

🎧 Episode 142 – How Much You Pay in Taxes in California from $300K to $1.5M (It Gets Worse)

Prefer to watch or listen?

Watch on YouTube: EP 142 – How Much You Pay in Taxes in California Listen on Apple Podcasts: EP 142 on Buzzsprout

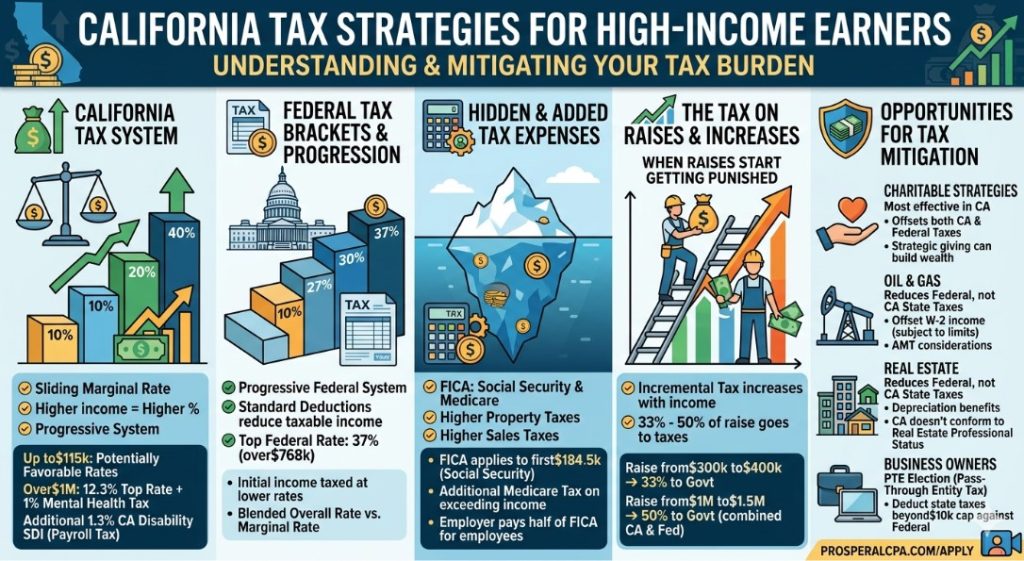

California’s Tax System: More Layers Than You Think

Most states operate on a flat income tax — somewhere between 4% and 6%, regardless of how much you earn. California is different. It runs a steeply progressive marginal rate that climbs all the way to 12.3% for incomes above $1.48 million.

But the headline rate isn’t the whole story. Layered on top of the 12.3% are two taxes most people don’t see coming:

The Mental Health Services Tax adds 1% on income above $1 million. That pushes your top California marginal rate to 13.3%.

California State Disability Insurance (SDI) adds another 1.3% on all wages. This one doesn’t even show up on the income tax schedule — it hits your paycheck as a payroll deduction.

Combined, the effective top California state tax rate for a high earner is 14.6% — before a single dollar goes to the federal government.

The Federal Side Is No Better

At the federal level, the top marginal income tax rate is 37% for income above $768,000 (married filing jointly, 2026). But the real rate is higher than that. The Net Investment Income Tax adds 3.8% on investment income above certain thresholds, and the additional Medicare tax adds 0.9% on earned income above $200,000 for single filers ($250,000 married). For employees, the effective federal ceiling is closer to 39%. For the self-employed without an S corporation structure, it can exceed 40%.

Stack California’s 14.6% on top of the federal burden, and you begin to understand why high earners in the state feel like they’re running in place.

Your Real Tax Bill at Every Income Level

The following figures are based on actual mock tax returns run through professional tax software for a married couple filing jointly in California. These numbers reflect 2025 rates but remain highly relevant for 2026 and beyond.

$300,000 — The Entry Point

At $300K, a married couple pays approximately $51,000 in federal taxes and $19,000 to California, for a total of around $70,000. The blended state rate at this level is 6% — higher than most states, but not alarming. The marginal rate on raises at this income band is 33%.

$400,000 — The Threshold That Matters

At $400K, the total combined tax bill hits $100,000. Federal comes to $74,000; California adds $28,000 at a blended 7% state rate.

This is the threshold where advanced tax planning starts to make serious economic sense. Below $100,000 in total taxes, many of the more powerful reduction strategies don’t generate enough savings to justify their cost or complexity. At $400K in California, they do.

It’s also where the tax code starts penalizing success more aggressively. Above this income level, the QBI deduction (worth up to 20% of qualified business income) begins to phase out for married filers. The child tax credit disappears. And the federal bracket jumps from 24% to 32% on income above $400K.

Of that $100,000 raise from $300K to $400K, $33,000 goes directly to government. A third of every incremental dollar earned.

$500,000 — 41% of Your Raise Is Gone

The blended rate rises to 29% at $500K. More telling: of the $100,000 raise from $400K to $500K, $40,755 goes to taxes. Take-home from that raise is only about $60,000. Welcome to the phase-out zone where losing deductions and crossing brackets collide.

$750,000 — You Think You Made $750K. You Didn’t.

At $750,000, the blended rate reaches 34%. Of the additional $250,000 earned from $500K to $750K, $112,000 — 45% — goes to taxes.

After federal and state taxes, a $750,000 earner takes home approximately $493,000. And that doesn’t account for the SDI payroll tax, Medicare surtax, property taxes, or sales taxes — all of which run above the national average in California. The real after-tax number is meaningfully lower than $493,000.

$1,000,000 — Almost Half Your Raise Vanishes

At $1 million, the blended rate is 38%. On the jump from $750K to $1M, 48% of that $250,000 raise goes to taxes. Being a seven-figure earner in California means losing nearly half of every incremental dollar to the government.

$1,500,000 — 50% of Your RSU Vest Goes to Taxes

At $1.5 million, California’s blended state rate reaches 10%. Add 32% in federal taxes and the combined blended rate is 42%. But look at the marginal impact: of the $500,000 increase from $1M to $1.5M — whether from a raise, a bonus, or RSU vesting — more than 50% goes to federal and state taxes. Every other dollar earned at this level is absorbed by the government.

This is where the alarm bells have to ring. And this is exactly why proactive tax planning isn’t optional at these income levels.

Want to know how much you could save in taxes?

Apply for a free tax strategy consultation and we’ll show you exactly what’s possible based on your income and situation.

→ Apply here: https://prosperlcpa.com/apply

What You Can (and Can’t) Do to Fix This in California

California doesn’t conform to several federal tax provisions that make some of the most popular strategies far less effective for state purposes. Understanding these limits is critical before choosing a path.

Oil and Gas: Useful, But Limited in California

Oil and gas investments are one of the most powerful tax reduction tools available to high W-2 earners at the federal level. Intangible drilling costs can generate significant deductions in the year of investment, and the passive income they generate pairs well with other strategies.

The problem in California: oil and gas operations are domiciled in Texas, North Dakota, or other producing states — not California. That means the deductions offset federal taxes but not California state taxes. California won’t allow them.

Additionally, for high W-2 earners, the excess business loss limitation caps deductions at $512,000 for married filers ($256,000 single) in 2026. And the alternative minimum tax can further erode the benefit.

That said, oil and gas still makes strategic sense for California earners in the $500K–$600K income range. At that level, creating a $50,000–$100,000 business loss can phase a filer into eligibility for an additional SALT deduction — unlocking up to $30,000 more in state tax deductions against federal income. A $100,000 oil and gas deduction can effectively function as a $130,000 deduction when it triggers this SALT benefit. That’s a meaningful outcome.

Real Estate Professional Status: California Doesn’t Recognize It

For real estate investors, Real Estate Professional Tax Status (REPS) is a powerful tool. It allows qualifying taxpayers to treat rental losses as non-passive and offset W-2 income — often generating six-figure deductions through accelerated depreciation.

California does not conform to REPS. Losses created through this strategy will offset federal taxes but not California state taxes. For a $1M earner who generates $500,000 in real estate losses, the California tax bill remains largely unchanged.

The only real estate path to California state tax reduction is short-term rentals in California — but those come with active management requirements and California-specific compliance complexity. It’s not off the table, but it requires careful structuring.

California also does not allow 100% bonus depreciation. Depreciation-based deductions are spread over longer recovery periods on the state return, significantly reducing the immediate impact of cost segregation and similar strategies.

Charitable Strategies: The Most Effective Tool for California Residents

If you’re a high earner in California and you want to reduce both your federal and state taxes meaningfully, strategic charitable giving is the most powerful lever available.

Unlike oil and gas or real estate losses, properly structured charitable deductions offset both federal and California taxable income. The strategies range from conservative to more aggressive, including:

- Donor-advised funds for appreciated assets

- Charitable remainder trusts for estate planning and income generation

- Conservation easements and resource-based partnerships for larger deduction multiples (these require careful vetting and carry more audit risk)

The math on charitable strategies is striking. For a California earner at $1.5 million, a well-executed charitable strategy can reduce taxable income from $1.5M down to $750,000. At that level, total taxes drop to approximately $256,000 — an effective rate of 17% on gross income, down from 42%. That’s not a rounding error. That’s a transformation.

Stack $512,000 in business losses on top of the charitable reduction, and taxable income can compress down to the $200,000–$300,000 range on the federal side.

Pass-Through Entity Tax Election for Business Owners

California business owners have an additional tool: the Pass-Through Entity (PTE) tax election. This allows S corps and partnerships to pay California state income taxes at the entity level and deduct them against federal income — bypassing the $10,000 SALT deduction cap that applies to individuals.

For a California business owner earning $1.5 million, this election can unlock up to $149,000 in additional federal deductions. It’s one of the highest-impact, lowest-complexity strategies available to California business owners and should be evaluated annually.

Timing Your Exit: Deferred Income and Relocation

For those who may eventually retire outside California — whether to Florida, Texas, Nevada, or elsewhere — income timing becomes a powerful planning tool. California taxes 401(k) and IRA distributions as ordinary income. It also taxes capital gains at ordinary income rates, unlike the favorable federal long-term capital gains treatment.

If you know you’ll leave California at some point, defer as much taxable income as possible until after you establish residency elsewhere. Don’t take 401(k) distributions. Don’t sell appreciated stocks. Don’t trigger RSU vestings if you can time them. Every dollar of deferred income recognized after leaving California avoids the state’s top rates entirely.

FAQ

At what income level does it make sense to start advanced tax planning in California? Once your combined federal and state tax bill exceeds $100,000 — typically around $400,000 in California for married filers — the more sophisticated reduction strategies begin to generate meaningful returns that justify their cost and complexity.

Does California allow oil and gas deductions against state taxes? No. Oil and gas deductions offset federal taxes only. California does not recognize these losses because the operations are domiciled in other states. There are scenarios where oil and gas still makes strategic sense for California residents in the $500K–$600K range by unlocking SALT deductions, but the state-level benefit is not direct.

Can I use Real Estate Professional Tax Status to reduce my California taxes? No. California does not conform to REPS. Losses generated through this designation will reduce your federal taxable income but have no impact on your California state tax bill. Short-term rental losses domiciled in California may offer a partial workaround.

What is the most effective strategy for reducing taxes in California? For most high W-2 earners, strategic charitable deduction strategies are the most effective because they offset both federal and California state taxes simultaneously. Business owners also benefit significantly from the pass-through entity tax election.

What is the PTE election and who qualifies? The Pass-Through Entity tax election allows California S corporations and partnerships to pay state income taxes at the entity level, making those taxes fully deductible against federal income. This bypasses the $10,000 SALT cap. California business owners should evaluate this annually with their CPA.

Does California tax capital gains the same as ordinary income? Yes. California taxes long-term capital gains at the same rates as ordinary income. There is no preferential capital gains rate at the state level, unlike the federal system.

What is the excess business loss limitation for W-2 earners? In 2026, the maximum business loss a married W-2 earner can use to offset non-business income is $512,000 ($256,000 for single filers). Business owners face no such cap — they can offset all business income with business losses.

Is it worth moving to Texas or another no-income-tax state? It may be — but run the numbers before you decide. In many cases, the combination of California’s earning potential and a well-executed tax reduction strategy produces better after-tax results than relocating. For a $1.5M earner, slashing effective taxes from 42% to 17% while staying in California may outperform the net benefit of moving, once you account for lower income potential, relocation costs, and lifestyle changes.

Key Takeaways

- California’s effective top state tax rate reaches 14.6% when you include the mental health services surtax and SDI — before any federal taxes apply.

- At $400K income, a California married couple’s tax bill hits $100,000 — the threshold where advanced planning starts to make serious economic sense.

- From $400K to $500K, 41% of that raise goes to taxes. From $1M to $1.5M, it’s over 50%.

- Oil and gas deductions are powerful federally but do not reduce California state taxes — with a narrow exception for earners at $500K–$600K who can unlock SALT benefits.

- California does not recognize Real Estate Professional Tax Status. Real estate losses through REPS offset federal income only.

- Charitable deduction strategies are the most effective tool for California residents because they offset both federal and state taxes simultaneously.

- A $1.5M earner who executes a full charitable + business loss strategy can reduce their effective tax rate from 42% down to 17%.

- The PTE election is a high-impact, underused strategy for California business owners that unlocks significant additional federal deductions beyond the SALT cap.

- If you plan to retire outside California, defer taxable income — including 401(k) distributions, stock sales, and RSU vestings — until you’ve established residency in a lower-tax state.

- Before relocating, model what advanced tax planning could achieve. Moving may not be necessary — or optimal.

Ready to See How Much You Could Save?

Apply for a free tax strategy consultation: → https://prosperlcpa.com/apply

Not ready yet? Start with our free Tax Planning Checklist and mini-course: → https://taxplanningchecklist.com

This article is adapted from Episode 142 of the Mark Perlberg CPA Podcast.Watch on YouTube: EP 142 – How Much You Pay in Taxes in California from $300K to $1.5M Listen on Apple Podcasts: EP 142 on Buzzsprout